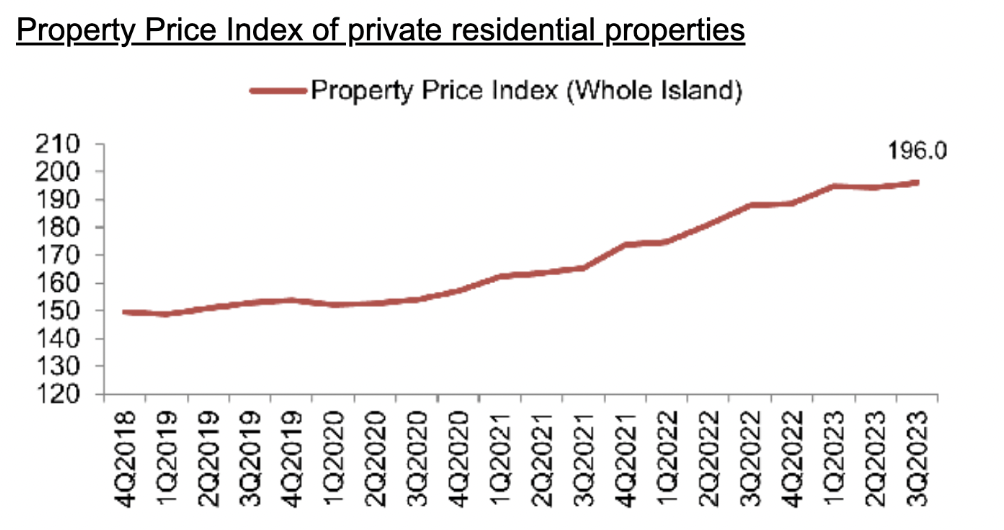

Prices of private residential properties increased by 0.8% in Q3 2023 following a 0.2% decline in the previous quarter.

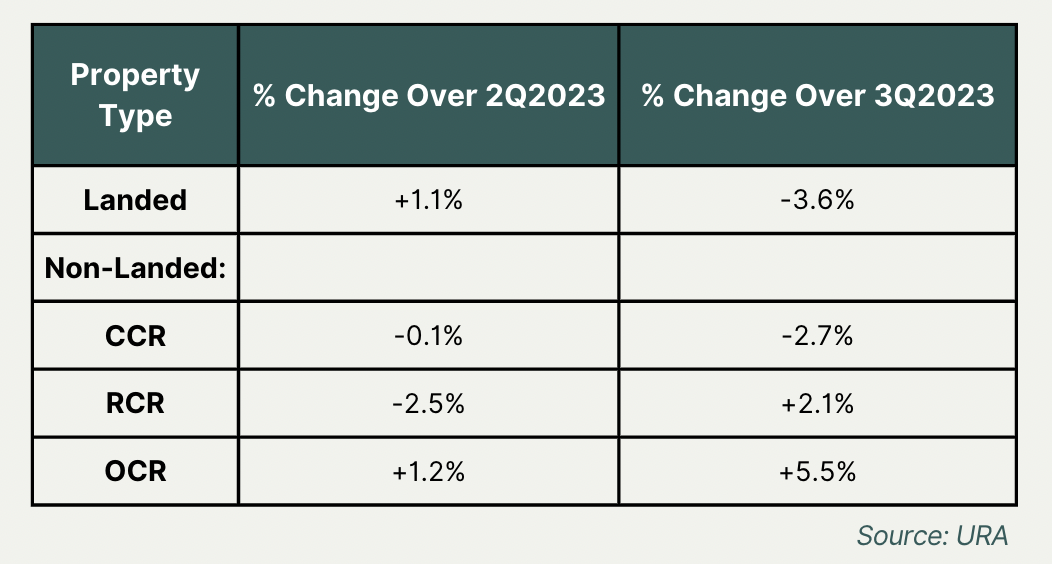

The overall price increase of 0.8% was led by a gain in prices of non-landed OCR and RCR properties.

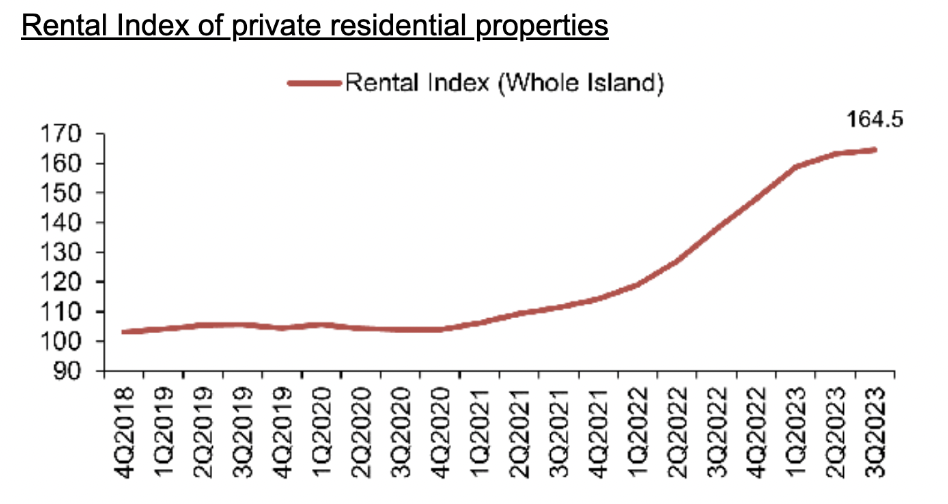

Rentals of private residential properties increased by 0.8% in 3rd Quarter 2023, again lower than the 2.8% increase in the previous quarter, and 7.2% in Q1.

Overall Increase in Volume of Transactions:

- 2,900 resale/subsale transactions in 3Q2023, compared with the 2,976 units transacted in the previous quarter.

- This tells us that market demand remains strong.

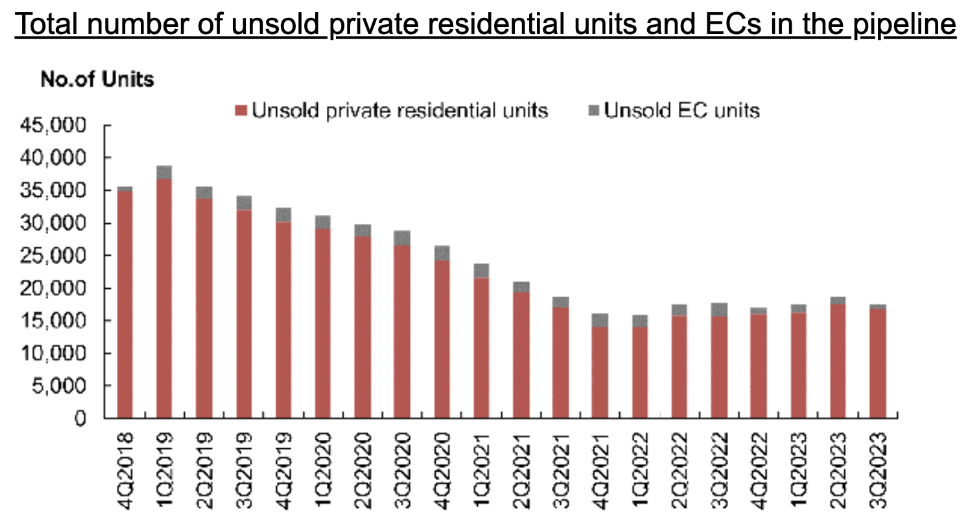

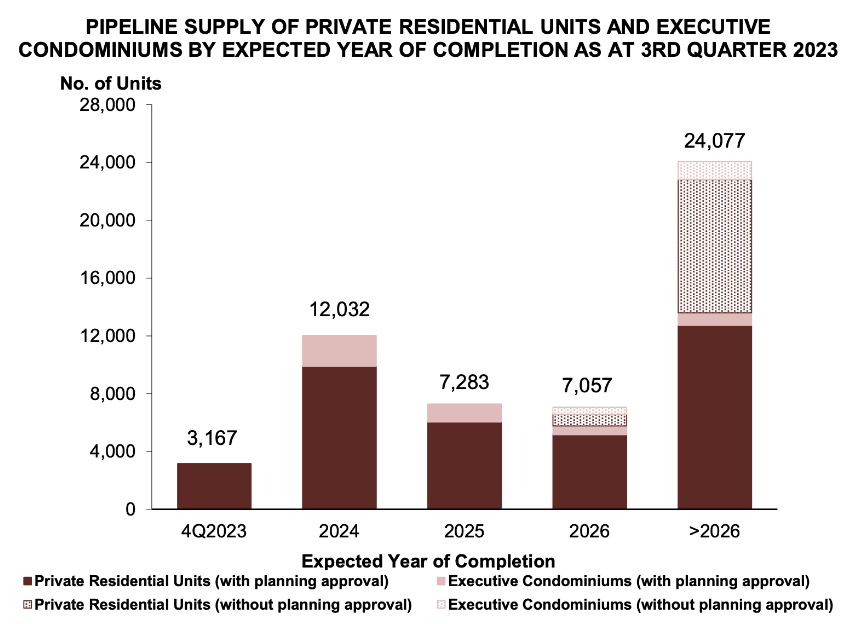

As at the end of Q3 2023, there was a total supply of 41,851 uncompleted private residential units (including ECs) in the pipeline with planning approvals, of which 17,576 units remained unsold.

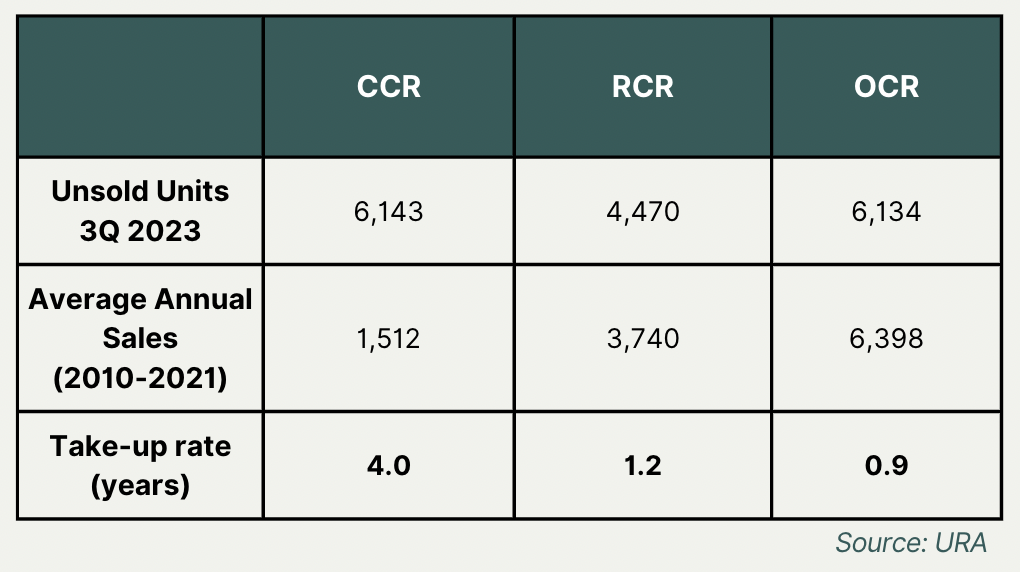

Too much supply?

Not in the RCR and OCR.

Overall unsold private housing supply (new launch) is still tight within these areas and are expected to sell out within a year’s time.

- In total, around 20,400 units (including ECs) are expected to be completed in 2023.

- This would be the highest annual private housing supply completion since 2017.